Introduction

Are membership savings programs worth it? This question has become increasingly common as subscription-based discount platforms expand across travel, retail, dining, and essential services. Membership savings programs promise structured discounts across travel, retail, dining, and essential services. In exchange for a recurring fee, consumers gain access to negotiated pricing networks, cashback structures, or aggregated purchasing power.

The central question is not whether discounts exist, but whether the overall structure delivers measurable value relative to cost. Determining whether membership savings programs are worth it requires examining usage patterns, fee structures, category alignment, and long-term sustainability.

What “Worth It” Actually Means

Many consumers ask, are membership savings programs worth it, especially when subscription fees are involved, so when evaluating whether a membership savings program is worth it, the analysis should focus on net financial impact.

A program may offer legitimate discounts but still fail to generate net value if:

-

Membership fees exceed annual savings

-

Usage frequency is low

-

Savings apply primarily to infrequent categories

-

Pricing transparency is limited

“Worth it” should be defined as:

Annual Savings – Membership Cost = Net Positive Outcome

Anything else is marketing interpretation.

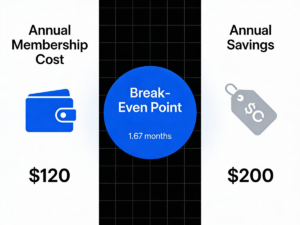

Break-Even Analysis as a Decision Tool

One of the most effective tools in evaluating membership savings programs is break-even analysis.

For example:

If a membership costs $120 annually and average per-use savings are $20, a member must use the program at least six times per year to justify the fee.

If actual usage averages three times annually, the program produces a net loss despite offering valid discounts.

Break-even modeling shifts the focus from advertised percentage savings to realistic behavioral alignment.

Modeling Realistic Usage Scenarios

Break-even analysis is only as accurate as the assumptions used to calculate it. Many consumers estimate usage optimistically when evaluating membership savings programs.

To improve accuracy, consider modeling three scenarios:

Conservative Scenario

Assume lower-than-expected usage frequency. For example, if you expect to use the program eight times annually, model it at five.

Moderate Scenario

Use realistic, past-year spending behavior as the baseline.

Optimistic Scenario

Model the highest plausible usage without assuming extraordinary changes in behavior.

Comparing these scenarios reveals whether savings are stable across realistic variations or dependent on ideal conditions.

Programs that only produce value under optimistic assumptions may carry higher behavioral risk.

When Membership Savings Programs Tend to Be Worth It

Membership savings programs are more likely to deliver net value when:

-

Travel is frequent and predictable

-

Retail spending is consistent

-

Dining expenses are recurring

-

Utility or telecom categories are included

-

Members actively compare pricing before purchase

High-frequency categories improve the probability of exceeding break-even thresholds.

Households with structured spending habits often benefit more than irregular spenders.

When They May Not Be Worth It

Membership savings programs may underperform when:

-

Usage is sporadic

-

Spending categories are narrow

-

Membership costs are high relative to income

-

Savings rely on limited vendor participation

-

Discounts are comparable to public promotions

In some cases, publicly available promotional pricing may match or exceed membership discounts without requiring a subscription fee.

Psychological Factors in Perceived Value

Perceived value is often influenced by psychological bias rather than actual net savings.

Common influences include:

-

Optimism bias regarding usage frequency

-

Overweighting maximum advertised savings

-

Underestimating membership fees

-

Emotional response to exclusivity language

Consumers may feel value simply from access, even when financial outcomes are neutral or negative.

A disciplined savings comparison approach reduces these biases.

Category Concentration Risk

Programs heavily concentrated in one category, such as travel, may require high usage within that category to justify cost.

Diversified category coverage — including retail, dining, and essential services — reduces dependency on a single behavior pattern.

However, broader category lists do not automatically guarantee better value. Depth and usability matter more than category count.

Vendor Participation and Accessibility

A savings program may advertise strong category coverage, but vendor participation levels can significantly influence actual usability.

Questions to consider include:

-

Are savings available nationwide or limited to specific regions?

-

Are participating vendors mainstream or niche providers?

-

Are discounts automatic, or do they require manual claim processes?

-

Are exclusions common during peak seasons?

High theoretical savings are less meaningful if vendor accessibility is limited.

Evaluating accessibility prevents overestimation of practical savings potential.

Regulatory and Market Constraints

Savings programs operating in regulated sectors such as utilities or telecommunications may offer incremental rather than dramatic savings.

State-level regulation can limit pricing flexibility, meaning savings are often optimization-based rather than discount-based.

Consumers should distinguish between:

-

Negotiated discount pricing

-

Rate optimization

-

Cashback rebate models

Understanding these distinctions prevents inflated expectations.

Utilities pricing in many states is regulated at the state level through public utility commissions.

Fee Structure and Renewal Considerations

Membership savings programs often operate on automatic renewal models. While this provides convenience, it also introduces the possibility of unused renewals.

Before enrolling, consumers should evaluate:

-

Renewal notification policies

-

Refund eligibility windows

-

Contract length requirements

-

Price increases after introductory periods

Programs with transparent renewal practices reduce friction and long-term dissatisfaction.

Annual value should be reassessed before each renewal cycle. Understanding how membership savings programs work is essential before determining whether they are worth it

Long-Term vs Short-Term Value

Temporary promotional discounts can sometimes exceed membership savings in isolated transactions.

However, evaluating worth requires annualized analysis rather than isolated examples.

A consistent 10–15% discount applied repeatedly may produce greater annual savings than an occasional 40% promotional event.

Long-term modeling provides a more reliable decision framework.

Who Should Consider Membership Savings Programs

Membership savings programs may be suitable for:

-

Households with predictable spending

-

Frequent travelers

-

Consumers comfortable with subscription models

-

Individuals willing to calculate break-even thresholds

They may be less suitable for:

-

Low-frequency spenders

-

Households with minimal discretionary spending

-

Consumers who rely primarily on public promotions

Suitability depends more on behavioral alignment than advertised discount size.

A Structured Decision Framework

To determine whether a membership savings program is worth it, consider the following structured process:

-

Identify annual membership cost

-

Estimate realistic usage frequency

-

Calculate break-even threshold

-

Compare against public promotional pricing

-

Evaluate transparency of terms

-

Assess long-term sustainability

Determining whether a membership savings program is worth it requires structured comparison rather than assumption. For a deeper explanation of how programs are analyzed, see our evaluation methodology. Applying consistent criteria reduces reliance on marketing claims.

Comparing Membership Savings to Alternative Strategies

Membership savings programs are only one approach to cost reduction. Alternatives include:

-

Public promotional tracking

-

Cashback credit cards

-

Bulk purchasing strategies

-

Loyalty program stacking

-

Seasonal purchasing planning

In some cases, combining moderate membership savings with strategic promotional timing may produce stronger outcomes than relying on either strategy alone.

A disciplined savings comparison approach evaluates all available tools rather than assuming membership enrollment is the optimal solution. Consumers can compare retail pricing through publicly available sources such as the U.S. Bureau of Labor Statistics.

Frequently Asked Questions

1. Are membership savings programs worth the cost?

Membership savings programs can be worth the cost if annual savings exceed the membership fee. This typically depends on usage frequency, category alignment, and break-even thresholds. Consumers who travel frequently or make recurring retail purchases may realize measurable value, while infrequent users may not exceed the annual cost.

2. How do you calculate whether a savings membership is worth it?

The most effective method is break-even analysis. Divide the annual membership fee by the average savings per transaction to determine how many uses are required to justify the cost. If actual usage falls below that threshold, the membership does not generate net value.

3. Are membership savings better than public promotions?

In some cases, public promotional pricing may match or exceed membership discounts. However, membership savings programs may provide consistent pricing advantages across multiple transactions, whereas promotions are often temporary. A structured comparison is required to determine relative value.

4. Who benefits most from membership savings programs?

Households with predictable spending patterns, frequent travelers, and consumers comfortable with subscription models tend to benefit most. Individuals with irregular or low discretionary spending may find it more difficult to exceed break-even thresholds.

Conclusion

Membership savings programs can deliver measurable value under the right conditions. However, they are not universally beneficial, nor are advertised discounts sufficient proof of financial advantage.

Determining whether membership savings programs are worth it requires structured comparison, conservative modeling, and alignment with actual spending behavior.

Ultimately, determining whether membership savings programs are worth it depends on disciplined break-even analysis rather than advertised discount percentages. Savings Governance encourages disciplined evaluation rather than assumption-based enrollment.