Introduction

Membership savings programs have grown rapidly across travel, retail, dining, and essential services in the United States. These programs promise structured discounts and negotiated pricing in exchange for access through subscription or registration.

Understanding how membership savings programs operate requires examining their pricing structure, funding model, and long-term value proposition rather than focusing solely on advertised percentage discounts.

The Evolution of Membership Savings in the United States

These savings platforms did not emerge from traditional coupon marketing. They evolved from corporate purchasing agreements, wholesale distribution networks, and negotiated pricing systems designed for large organizations.

Over time, digital platforms adapted these models for individual consumers by aggregating purchasing demand. Instead of relying on one employer or company, platforms group thousands of members together to increase bargaining power.

This shift has led to the growth of consumer-access membership models across:

-

Travel and hospitality

-

Online retail

-

Subscription services

-

Utilities and telecommunications

Understanding this historical shift clarifies why membership savings programs operate differently from promotional discount platforms.

Cost Structures and Consumer Psychology

Membership savings programs rely on predictable consumer behavior. When consumers commit to a recurring fee, platforms gain:

-

Revenue stability

-

Negotiation leverage

-

Long-term vendor relationships

However, consumers often overestimate projected savings due to:

-

Optimism bias

-

Misinterpretation of “up to” percentages

-

Failure to calculate break-even points

-

Irregular usage patterns

A disciplined evaluation process prevents psychological overcommitment.

Regulatory and Industry Constraints

Not all categories allow unlimited pricing flexibility.

For example:

-

Utilities are often regulated at the state level.

-

Telecommunications pricing may include mandated fees.

-

Travel pricing fluctuates seasonally.

These structural constraints influence how much savings a membership program can realistically generate.

Programs operating in highly regulated industries must work within those boundaries, limiting exaggerated claims but potentially offering incremental optimization. Utility pricing is often governed at the state level through public utility commissions.

Long-Term Value vs Short-Term Promotions

Consumers frequently compare membership programs against temporary sales. However, temporary promotions may not reflect annualized pricing advantages.

For example:

A one-time 50% promotional discount does not necessarily outperform a consistent 10–20% negotiated rate applied repeatedly across the year.

Long-term savings evaluation should be based on:

-

Annual spending totals

-

Category frequency

-

Repeatability of discounts

-

Membership cost amortization

This long-term framing provides more accurate outcomes.

The Difference Between Promotional Discounts and Structural Savings

Not all discounts are structured the same way. Promotional discounts are typically short-term incentives designed to stimulate demand. These include limited-time sales, coupon codes, or clearance pricing.

Structural savings, by contrast, are built into negotiated pricing systems. Membership savings programs attempt to offer structural savings by leveraging aggregated demand rather than temporary promotions.

This distinction matters because promotional discounts may appear larger in percentage terms but lack repeatability. Structural savings aim to provide more consistent pricing advantages over time.

Households evaluating membership savings programs should distinguish between:

-

Promotional marketing events

-

Long-term negotiated pricing

-

Cashback or rebate models

-

Corporate-style access pricing

Understanding this difference reduces reliance on headline percentages and focuses on predictable outcomes.

What Is a Membership Savings Program?

A savings program for member groups provides consumers access to negotiated pricing or structured discounts through a recurring membership or access model.

Unlike traditional coupons, these programs aim to provide:

-

Repeatable savings

-

Negotiated pricing tiers

-

Aggregated purchasing power

-

Access to non-public rate structures

Their effectiveness depends heavily on usage frequency and category alignment.

How Pricing Is Structured

Membership savings platforms typically operate using one or more of the following models:

Subscription-Based Access

Consumers pay a recurring fee to access negotiated discounts across categories.

Cashback or Rebate Systems

Savings are applied after purchase in the form of partial refunds or credits.

Corporate-Style Pricing

Platforms negotiate pricing structures traditionally available to large organizations and extend access to individual members.

Each model carries different break-even considerations. Consumer pricing trends can be tracked through sources such as the U.S. Bureau of Labor Statistics.

Revenue Models Behind Membership Savings Platforms

To understand how membership savings programs operate, it is important to examine how platforms generate revenue.

Most membership-based platforms rely on one or more of the following models:

Membership Fees

Recurring subscription fees provide predictable platform revenue.

Commission Structures

Platforms may receive commissions from partner vendors when members make purchases.

Aggregated Purchasing Agreements

Large member pools increase negotiating leverage with suppliers.

These revenue structures do not automatically invalidate savings. However, understanding them helps consumers evaluate incentives and sustainability.

Transparency in revenue design is often a signal of platform maturity.

Industry Examples of Membership Savings Categories

While specific offerings vary by platform, membership-based savings programs commonly operate within the following sectors:

Travel and Accommodation

Negotiated hotel rates, bundled packages, and access to wholesale pricing structures.

Retail and Online Shopping

Preferred pricing networks, partner discounts, or cashback arrangements.

Dining and Local Services

Location-based discounts and membership dining networks.

Utilities and Telecommunications

Emerging partnerships in electricity, gas, internet, and mobile services, often dependent on regional regulation.

Savings consistency varies by industry due to pricing complexity and regulatory frameworks.

Where Membership Savings Are Most Common

Membership-based savings programs are most frequently applied in:

-

Travel and hotel bookings

-

Retail and online shopping

-

Dining and lifestyle services

-

Utilities and telecommunications (emerging category)

Savings consistency varies significantly by industry.

Evaluating Real Savings

To evaluate whether a membership savings program delivers measurable value, households should consider:

-

Annual membership cost

-

Realistic usage frequency

-

Category relevance

-

Transparency of pricing structure

-

Break-even thresholds

For a detailed explanation of how these calculations are applied across platforms, see our evaluation methodology. Short-term promotions should not be confused with long-term structural savings.

Common Misconceptions

“Higher advertised discounts mean better value.”

Advertised percentages often represent maximum theoretical savings, not typical outcomes.

“All households benefit equally.”

Savings effectiveness varies by spending pattern.

“Membership savings replace price comparison.”

Independent comparison remains essential.

Key Indicators of a Sustainable Savings Program

When evaluating discount savings programs, look for:

-

Clear fee disclosure

-

Transparent partner lists

-

Realistic savings examples

-

Stable pricing structure

-

Multiple savings categories

Programs relying heavily on aggressive marketing rather than structural transparency may require additional scrutiny.

When Subscription-Based Discounts Are Most Effective

Membership savings programs tend to perform best when:

-

Households travel multiple times per year

-

Discretionary spending is predictable

-

Members actively compare pricing

-

Programs align with high-spend categories

A broader discussion of whether these models provide measurable value can be found in our guide on whether membership savings programs are worth it.

They tend to underperform when:

-

Usage is infrequent

-

Spending patterns are irregular

-

Membership fees exceed realistic annual savings

Effectiveness depends less on advertised percentages and more on behavioral alignment.

Frequently Asked Questions

1. How do membership savings programs generate discounts?

Membership savings programs typically generate discounts through negotiated vendor agreements, aggregated purchasing power, commission-sharing models, or cashback systems. The underlying mechanism determines both the sustainability and depth of savings.

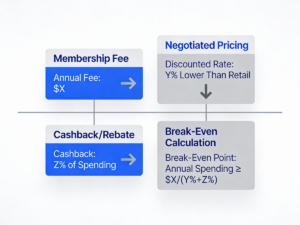

2. What is break-even modeling in a savings program?

Break-even modeling calculates how many transactions are required for total savings to exceed the membership fee. It provides a structured way to determine whether participation is financially justified.

3. Are membership savings programs subscription-based?

Most membership savings programs operate on subscription models, either monthly or annually. This recurring structure allows access to negotiated pricing networks and bundled savings categories.

4. Do all savings categories provide the same level of discount?

No. Discount depth varies by category, vendor participation, and regulatory environment. Travel and retail may offer stronger variability, while utilities and telecommunications often provide incremental savings due to regulatory constraints.

Final Considerations

Membership savings programs can provide value when aligned with household spending behavior. However, they require structured evaluation and realistic usage assumptions.

Savings Governance examines these programs through analytical comparison rather than promotional claims. For a detailed explanation of our analytical framework, review our evaluation methodology.